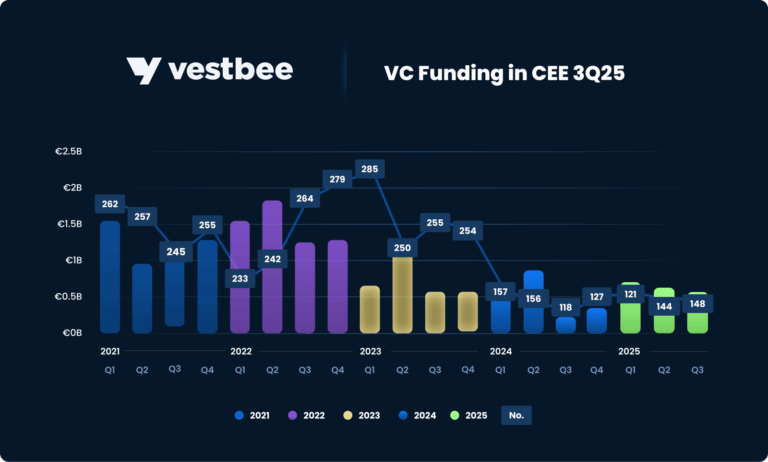

Vestbee, Europe’s leading platform connecting startups, VCs, accelerators, and corporates, has released its latest VC Funding in CEE report for Q3 2025, revealing a stable yet increasingly polarized venture capital landscape. While the total number of transactions in the region rose slightly to 148, overall investment volume dropped to just over €510 million, and almost half of that capital came from only three megadeals – MaintainX, Seon, and Spacelift. This capital concentration, however, was not unique to CEE, and it mirrored global trends, as investors worldwide lean heavily on proven category leaders – especially in hyped up markets like AI.

Uneven capital flows despite stable deal activity

In Q3 2025, startups across Central and Eastern Europe raised more than €510 million across 148 publicly reported rounds. This marks a slight increase in deal count compared to the previous quarter, though total capital invested fell by about 20% from Q2’s €640 million. Monthly activity ranged from 31 to 54 rounds, with a modest slowdown in August reflecting Europe’s traditional summer lull.

As in other regions, capital distribution was highly uneven. The largest disclosed rounds: MaintainX’s €129 million Series D, Seon’s €69 million Series C, and Spacelift’s €44 million Series C, together accounted for almost half of all regional investment.

Beyond these headline rounds, investment sizes remained modest, with only ten deals exceeding €10 million. Still, the steady deal flow and gradual increase in foreign investor participation reflect continued confidence in the region’s long-term potential.

“While a small number of large rounds drove total funding in the quarter, the underlying fundamentals of the CEE ecosystem are strengthening,” said Ewa Chronowska, CEO at Vestbee. “We continue to see steady deal flow, improving quality, and growing participation from foreign investors — all signs of long-term confidence in the region’s potential. Yet, excluding these few late-stage transactions reveals a structural imbalance: most capital still concentrates around a limited group of established scale-ups instead of being more evenly distributed across early- and growth-stage ventures”.

Regional leaders and sector dynamics

Poland, Estonia, and Ukraine led by deal count with 39, 25, and 24 transactions respectively, together representing more than half of all disclosed rounds. Investor focus mirrored global priorities, with AI, deeptech, hardware, financial services, SaaS, security, and healthtech ranking among the most active sectors.

Among the most active VC funds were both established regional players as well as fresh entrants on the scene, including Inovo VC, FIRSTPICK, Startup Wise Guys, Coinvest Capital, Kaya VC, Purple Ventures, Vinci S.A., Specialist VC, MOC VC, SmartCap, Movens Capital, and Early Game Ventures.

Europe and global context: concentrated growth amid renewed optimism

Global venture capital reached approximately $97 billion in Q3 2025, marking a 38% increase year over year and the fourth consecutive quarter above $90 billion. Much of this growth was concentrated: just 18 companies captured a third of total investment. AI led the way, attracting roughly $45 billion, or 46% of global VC, followed by hardware (€16.2 billion), healthcare and biotech (€15.8 billion), and financial services (€12 billion). Late-stage funding surged 66%, while early- and seed-stage activity remained steady, sustaining a robust pipeline of innovation. The US continued to dominate the landscape, accounting for nearly two-thirds of global venture investment, and renewed IPO activity signaled a cautious but growing investor confidence in large-scale tech ventures.

In Europe, startups raised $13.1 billion across more than 1,000 deals, reflecting a 22% year-over-year increase and steady quarterly performance. Early-stage funding remained the backbone of the ecosystem, making up roughly 60% of total investment, with strong momentum in AI, deeptech, and biotech. Notable rounds included France’s Mistral AI and the UK’s Nscale, while growth-stage funding totaled $5.4 billion across 75 deals. Early-stage activity itself expanded 31% year over year to $6.1 billion, led by Finland’s IQM Quantum Computers, Belgium’s Aerospacelab, and the UK’s CuspAI.

For a detailed breakdown of CEE’s Q3 2025 VC landscape, including sector-specific performance, investor activity, and emerging market dynamics, access the full report.

source: Vestbee

{kind=link}

{kind=link}

{kind=link}

{kind=link}